A modern financial dilemma: Will I retire before paying off my student loans?

-

Stacy Teicher Khadaroo Staff writer

Stacy Teicher Khadaroo Staff writer

Gina Armer had successfully funded two bachelor’s degrees and a master’s degree, so when she decided to start an evening doctoral program, she felt confident.

“I was thinking a PhD is my key to the world … [and that] when I graduated, paying back my student loans would be a piece of cake. I was five years into that degree before I discovered that not all PhDs are equal,” she says.

Why We Wrote This

How far into people’s lives should student debt reach? As the amount owed by older Americans climbs, questions arise about everything from effects on the economy to what supports are needed to help people get solvent.

Among debates heating up around college costs, the stories of older Americans – those trying to jump-start careers, or pay for their kids’ degrees – don’t usually take center stage. But they raise important questions about what it means for so much student debt to last longer into the arc of people’s experience. How is it affecting the economy and the number of years people feel impelled to work? What kinds of road maps and guardrails might be needed to help them get to a reasonable exit point?

“I beat myself up a lot, thinking, why did I take out those loans?” says Dr. Armer. “But it seemed like a logical thing at the time.”

After turning 65 last Christmas, C. Lynn Hawkins started collecting Social Security. She uses about half her monthly check to rent a small Chicago apartment for seniors.

She’s gotten used to calls from loan servicers for an educational debt she hasn’t been able to pay, but lately, letters from the government have come too, telling her that tax refunds and part of her Social Security check will be withheld.

“I was trying to better myself,” Mrs. Hawkins says about her decision in 2012 to enroll in a certified medical assistant program at a for-profit school advertised locally and on TV.

Why We Wrote This

How far into people’s lives should student debt reach? As the amount owed by older Americans climbs, questions arise about everything from effects on the economy to what supports are needed to help people get solvent.

The school promised students it would lead them to a job. But when she graduated in 2014, “it did not happen,” she says.

Instead, she was shocked to find out that within the paperwork, she had inadvertently agreed to a $30,000 loan. She found a job in public transportation on her own, but it didn’t pay enough to enable her to make sufficient payments.

“I’m not trying to get out of the student loan situation, but they need to make it affordable. … I’m 65,” she says with an exasperated sigh. “This is insane to me.”

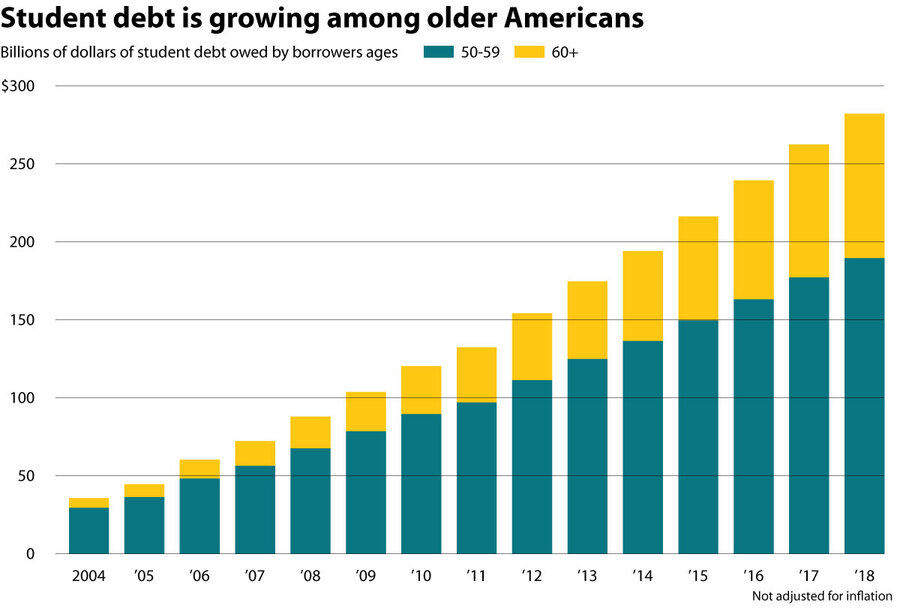

Americans over 50 now carry the fastest-growing balance of student loan debt. They number 8.4 million and account for about 20%, or $290 billion, of total student debt – a fivefold increase since 2004, the AARP Public Policy Institute reports.

Federal Reserve Bank of New York Consumer Credit Panel/Equifax

Call them the other seniors. Not the 20-somethings tossing their graduation caps into the air, but people who in theory should be laser focused on saving for retirement. Instead they have been trying to jump-start careers during a recession, or taking out gobs of money for their kids’ degrees, or still trying to pay off that loan from the 1980s that got out of control because plans went sideways.

Among debates heating up around college costs, the stories of older Americans don’t usually take center stage. But they raise important questions about what it means for so much student debt to last longer into the arc of people’s experience.

How is it affecting the economy and the number of years people feel impelled to work? How have family dynamics adjusted? As more people enter the wide ramps of access to college and financial aid, what kinds of road maps and guardrails might be needed to help them get to a reasonable exit point?

“Our society has perpetuated this idea, and there’s truth to it, that getting education is the key to social and economic mobility … [but] the stakes are higher than they are for almost any other type of debt,” says Persis Yu, director of the Student Loan Borrower Assistance Project at the National Consumer Law Center. Unlike those other debts, student loans can’t be discharged in bankruptcy.

“There is a point at which I think a society should just be more compassionate,” Ms. Yu says. “That’s somewhat the purpose of having Social Security, to ensure this safety in retirement, and student loan debt is threatening that for a lot of folks.”

Many people earn sufficient incomes to pay back loans without hardship. But default rates are higher as borrowers get older, with about 37% of those over 65 defaulting, and 5% of them – like Mrs. Hawkins – subject to the federal government taking “offsets” from Social Security or other sources, the Government Accountability Office reported in 2016.

The U.S. Department of Education has since told the school that Mrs. Hawkins attended that it cannot participate in the federal student aid system, partly because of misstatements it made about job placement rates. About 45% of borrowers who default attended for-profit colleges. Some borrowers are suing the department for its backlog of loan fraud claims. But the problem has been cyclical for decades. And that’s just one factor contributing to older Americans defaulting.

Second-guessing decisions

The first time Gina Armer earned a bachelor’s degree – in 1978 – she paid back her $10,000 loan in 10 years.

When she worked for Boeing, the company paid for her master’s degree. And after a voluntary layoff in the 1990s, she earned another bachelor’s to teach business to high schoolers. Soon after, she moved from Washington state to Idaho, where she taught at a community college and started an evening doctoral program in 2002.

At the time, she says, “I was thinking a PhD is my key to the world … [and that] when I graduated, paying back my student loans would be a piece of cake. I was five years into that degree before I discovered that not all PhDs are equal.”

It turned out that hers wasn’t the right kind for getting a university job that would pay her the $100,000 a year she had anticipated.

The recession struck before she finished in 2009. She delayed her payments for three years through forbearance, which caused her balance to grow to about $106,000. Her job paid $52,000 when she moved back to Washington.

Dr. Armer’s $400 monthly payments would have lasted until she was 85. But last year she was able to qualify for a loan-forgiveness plan because she teaches at a nonprofit university.

Now she’s expected to make $500 payments per month for 10 years and have the rest forgiven.

Such options don’t usually come up in conversations with colleagues, she says. “I think there’s a lot of shame, embarrassment about student loan debt for people that are as old as I am.”

Dr. Armer’s only dependent is her dog, but she’d love to be able to pay for a house or even just a car to replace her 2003 Jeep Liberty. She knows retirement is years away.

“It’s just such a trap,” she says. “I beat myself up a lot, thinking, why did I take out those loans? But it seemed like a logical thing at the time.”

Complicated rules

Part of the problem is a “confusing system,” the Institute for College Access & Success says in a recent report.

“Struggling borrowers often find themselves granted consecutive forbearances by their servicer,” even if they would do better in other plans, such as income-driven repayment that caps payments at a portion of salary each month, it notes. It recommends simplifying the array of such choices and helping servicers and borrowers understand them better.

Income-driven repayment is not available to people in default, however.

Senior citizens in default can have Social Security garnished – all but $750 of it each month. Despite the rise in the cost of living, that protected amount hasn’t been increased since 1996, Ms. Yu says.

These offsets pose a disproportionate hardship to people of color: 32% of whites, 52% of Latinos, and 45% of African Americans rely on Social Security for 90% or more of their income.

Sen. Ron Wyden of Oregon, the ranking member of the Senate Finance Committee, introduced a bill with some fellow Democrats in May that would prohibit Social Security garnishment.

One area of progress, Ms. Yu says: The Education Department has streamlined what had been an onerous process for people who qualify for disability discharges of their loans.

Parent-child dynamic

The idea of canceling student loan debt, proposed by some Democratic presidential candidates, wasn’t the go-to solution among older Americans in focus groups with Massachusetts Institute of Technology AgeLab researcher Julie Miller last year.

A few had the attitude of “What do I care. ... What are you, the government, going to take from me when I die with student loans?” she says of the study, which was sponsored by TIAA. Others told her they would feel proud when they’d finally paid off their debt, but they weren’t sure it was worth it.

For one segment of this age group, the student debt comes from financing education for their children or other relatives.

The sky’s the limit when it comes to federal Direct PLUS Loans for parents: They can borrow up to the full cost of the student’s attendance, without stringent assessment of their ability to pay the loans back.

“Often the choice of college becomes an emotional decision, but sometimes that comes at the expense of [parents’] own long-term financial security,” says Lori Trawinski, director of banking and finance at the AARP Public Policy Institute.

Another common way older adults help out is by co-signing a loan. One out of four people who co-signed ended up having to make payments because the borrower failed to do so, the AARP institute’s survey found.

Co-signers can request to be removed from most loans after a few years if the borrower has been making payments. But 71% of co-signers surveyed weren’t aware of this option.

Paying loans for their adult children had “changed the parent-child dynamic” for some parents, especially if the young adult was living at home after college without a job, says Ms. Miller, the researcher. They wondered if it had been wise to sacrifice their own retirement security.

The goal of highlighting these struggles is not to discourage people from taking on reasonable debt to obtain worthwhile education, but the effects of the student debt among baby boomers and millennials “can really ripple across generations,” Ms. Miller says. “We probably have not even seen the beginnings of the real ramifications just yet.”

Thanks to the dozens of readers who responded to our reader callout for stories about student debt. We included some of their responses in this piece. This is one of several audience-generated articles.